BrightSpire Capital (BRSP)·Q4 2025 Earnings Summary

BrightSpire Capital Q4 2025: Strongest Originations Quarter Since Restart, Dividend Yield at 11%

February 17, 2026 · by Fintool AI Agent

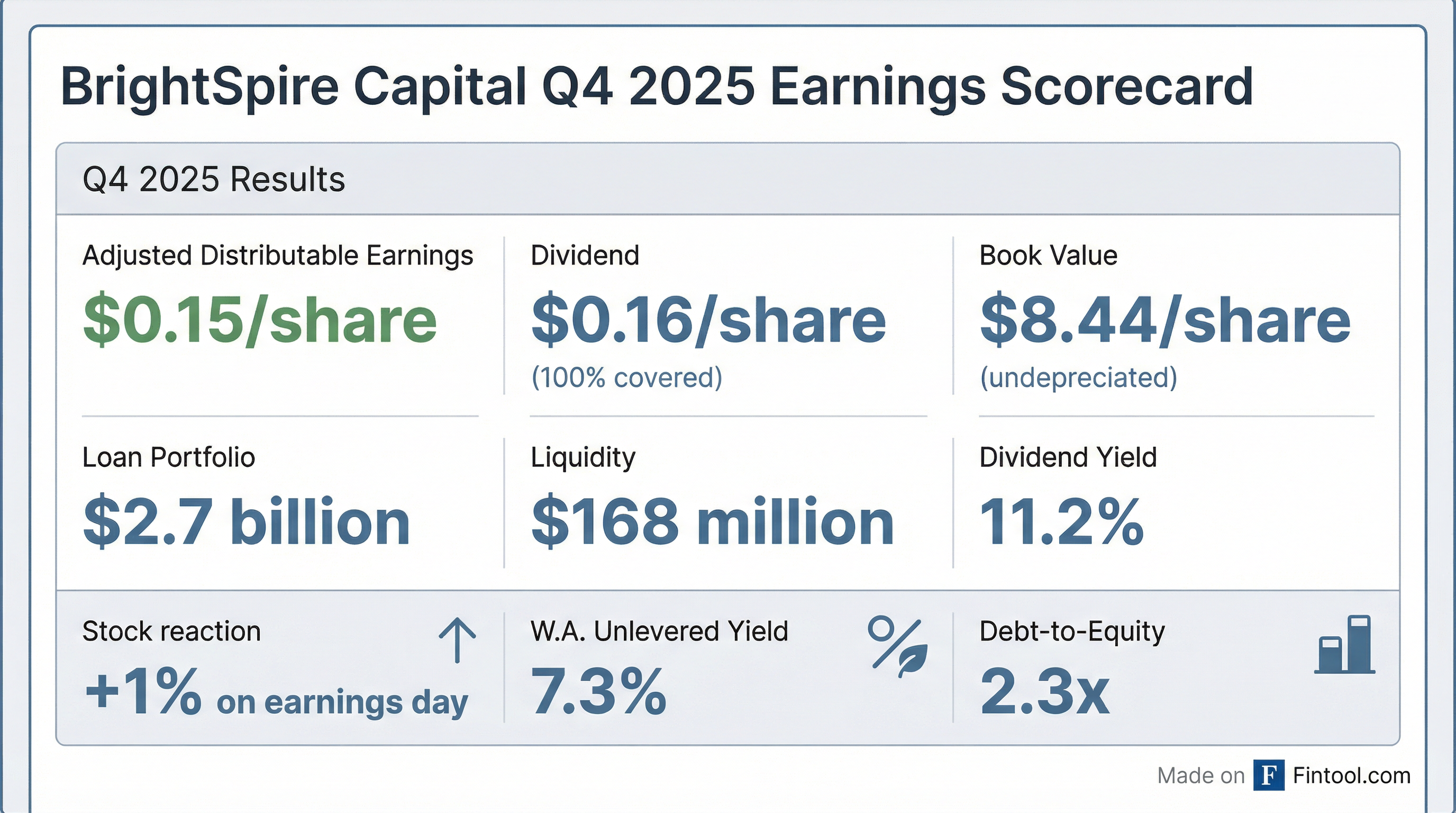

BrightSpire Capital (NYSE: BRSP) delivered its strongest quarter of loan originations since restarting originations in late 2024, committing $416 million across 13 new senior loans in Q4 2025 . The commercial real estate credit REIT reported Adjusted Distributable Earnings of $0.15 per share, supporting a $0.16 quarterly dividend that yields 11.2% annually .

The key story this quarter isn't earnings—it's balance sheet repositioning. Management is aggressively resolving problem loans and REO assets, with watchlist loans expected to drop 70% from $220 million to $66 million through early 2026 .

Did BrightSpire Beat Earnings?

BrightSpire reported Q4 2025 results slightly below analyst expectations on traditional metrics, though the company's preferred measure—Adjusted Distributable Earnings—came in at $0.15/share, covering 94% of the dividend .

GAAP net loss of ($0.12)/share was driven by:

- Real estate impairment of $8.0 million related to REO asset sales

- CECL reserve increase of $15.4 million for new originations

For the full year 2025, Adjusted Distributable Earnings totaled $0.64/share, exactly matching the $0.64/share in dividends paid .

What Changed This Quarter?

Three major developments stand out:

1. Originations Momentum

BrightSpire committed $416 million across 13 new senior loans in Q4—the strongest quarter since resuming originations . For full year 2025, the company committed $756 million across 26 loans .

Post-quarter, an additional $251 million was committed across 6 new loans .

2. Watchlist & REO Resolution

Management is accelerating the resolution of problem assets:

Watchlist Loans (starting at $220M) :

- One office loan and one industrial loan repaid ($42M)

- One multifamily loan foreclosed ($45M)

- Two multifamily loans expected to sell with repayment in Q1-Q2 2026 ($67M)

- Expected decline: 70% to $66M

REO Assets (starting at $315M) :

- Added one multifamily via foreclosure ($45M)

- One office property under contract (~$26M net proceeds)

- Two multifamily properties listed for sale

- Expected decline: 15% to $266M

3. New CLO Execution

Subsequent to quarter-end, BRSP closed a $955 million CLO with:

- 87.25% advance rate

- SOFR + 1.69% cost of funds

- $98M of available ramp-up proceeds

- 2.5-year reinvestment period

How Did Book Value Change?

Undepreciated book value declined from $8.68/share (Q3 2025) to $8.44/share (Q4 2025), driven by :

The real estate impairment was "largely driven by the decision to accelerate REO and watchlist resolutions and redeploy the capital," according to CEO Michael Mazzei .

At the current stock price of ~$5.80, BRSP trades at 69% of undepreciated book value—a significant discount that reflects investor caution around CRE credit.

What Does the Portfolio Look Like?

BrightSpire's $2.7 billion loan portfolio is heavily weighted toward multifamily (67%) with a conservative average loan size of $27 million .

Property Type Mix :

- Multifamily: 67%

- Office: 24%

- Mixed-use & Other: 8%

- Industrial: 1%

Geographic Concentration :

- West: 38%

- Southwest: 36%

- Northeast: 12%

- Southeast: 11%

- Midwest: 3%

The portfolio has been migrating toward multifamily—up from 51% in Q4 2024 to 67% today .

How Did the Stock React?

BRSP stock rose approximately 1% on earnings day, trading around $5.80 versus a prior close of $5.73. The muted reaction reflects:

- Results were largely in-line with expectations

- Book value decline was anticipated given REO resolution strategy

- 11%+ dividend yield provides support

Year-to-date, the stock is roughly flat, having traded in a range of $5.50-$6.00 since January.

What Did Management Say?

CEO Michael Mazzei's comments focused on the forward-looking opportunity:

"The Company had its strongest quarter of originations since restarting back in late 2024, successfully executed on a new CRE CLO and made substantial progress, including subsequent to quarter end, on the resolution of REO and watchlist loans."

"As we look ahead to 2026, our focus remains on growing the portfolio and earnings through new loan originations while continuing to resolve what remains of our REO and watchlist loans."

The tone was constructive, emphasizing:

- Portfolio growth through originations

- Problem asset resolution

- Capital redeployment into higher-yielding loans

Liquidity and Capitalization

BrightSpire maintains adequate liquidity with significant capacity to fund new originations:

The company also amended and extended its revolving credit facility to $120M (with accordion to $180M) through December 2028 , and upsized a master repurchase facility from $400M to $500M .

Key Risks and Concerns

1. Office Exposure — While multifamily is 67% of loans, office still represents 24% of the portfolio . Several office loans are on the watchlist or at risk rank 4-5.

2. Dividend Coverage — Q4 coverage of 94% was below 100% for the first time in 2025 . If earnings don't recover, the dividend could come under pressure.

3. Book Value Erosion — Undepreciated book value has declined from $8.75 in Q1 2025 to $8.44 in Q4 2025 . Continued impairments could further erode NAV.

4. Interest Rate Sensitivity — With 97% floating-rate loans, lower rates would compress net interest income. A 100bp rate cut would reduce annual net interest income by ~$2.5M ($0.02/share) .

Forward Catalysts

- Q1 2026 Resolution Progress — Management expects significant watchlist and REO resolution activity in Q1-Q2 2026

- Origination Pipeline — $251M already committed post-quarter; continued deployment would grow the portfolio

- CLO Ramp-Up — $98M of available ramp-up proceeds from new CLO provides dry powder

- Book Value Stabilization — If problem asset resolutions are completed, book value should stabilize

Key Takeaways

- Originations rebounding — $416M in Q4 was the strongest since restart, with $251M more post-quarter

- Problem asset resolution accelerating — Watchlist expected to decline 70%, REO down 15%

- Dividend maintained but tight — $0.16/share covered at 94% by Adjusted Distributable Earnings

- Significant discount to book — Stock trades at 69% of undepreciated book value

- 11%+ yield — Attractive income for investors willing to accept CRE credit risk

Earnings call scheduled for February 18, 2026 at 10:00 AM ET. Dial (833) 821-4389 or access webcast at brightspire.com.

Related Links: